This article is the second in a four-part series based on the book A Field Guide to Business Valuation, written by BerryDunn’s Seth Webber and Casey Karlsen.

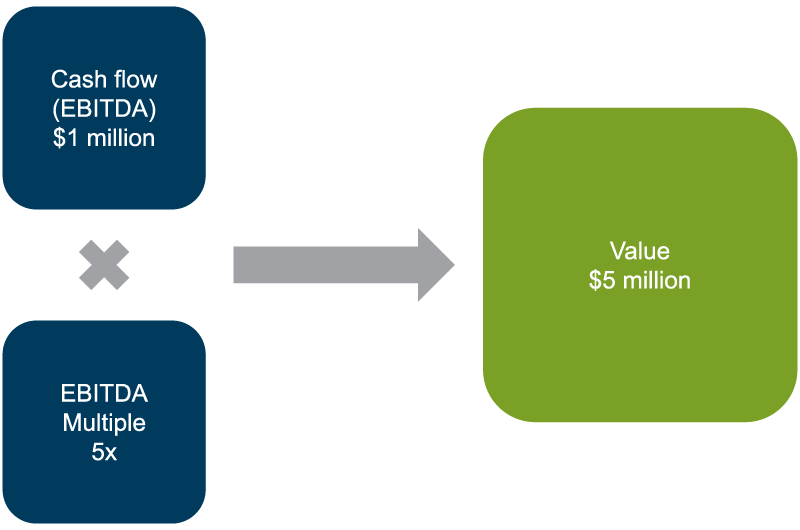

In Part I of this four-part valuation overview series, we talked about the “valuation rocket ship.” The valuation rocket ship is an illustration to conceptualize the components of a business valuation. The market approach, which we'll explore in this article, is one of three different ways to estimate the value of a company. In its simplest form, the market approach is fairly straightforward. Below is a very basic model for how a valuation could be applied:

This model is called the market approach because the EBITDA multiple is estimated based on a comparison to sales of similar companies.

Application of the market approach to valuation

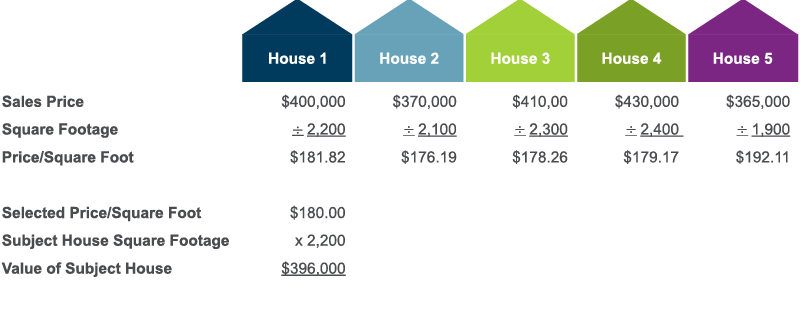

If you have ever had a house appraised, you have a level of familiarity with the market approach. When real estate appraisers value a house, they look for similar houses (i.e., comparables, or “comps”) that have sold and calculate the price per square foot of these comparables. They then select a reasonable price per square foot from the range indicated by the comparables and multiply this figure by the square footage of the house being valued, indicating its value.

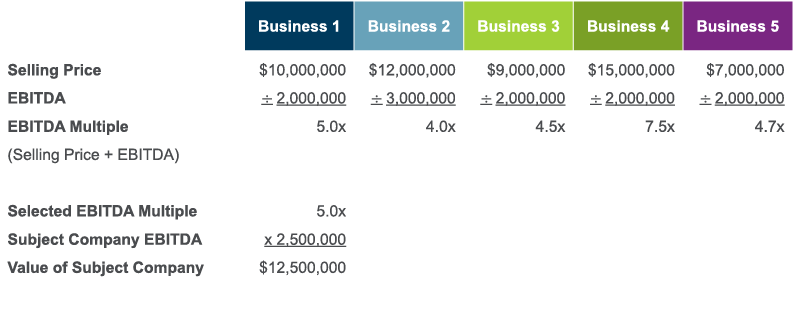

The market approach in business valuations follows the same basic procedures. However, price per square foot is not a meaningful indicator of business value. Extremely valuable businesses may have small facilities, and less valuable companies may have sprawling facilities. Therefore, instead of using a price per square foot, the valuation analyst uses more relevant denominators, such as annual revenue or EBITDA.

There are two primary market approach methods: the guideline completed transaction method and the guideline public company method. The guideline completed transaction method relies on the prices of recently sold similar companies, as illustrated in the example above. The guideline public company method uses the stock prices of similar publicly traded companies. By summing up the market value of all outstanding stock and debt, valuation analysts calculate the total value of publicly traded companies from the disparate ownership interests.

In both the guideline completed transaction method and the guideline public company method, the analyst performs the following steps:

- Identify sales of similar companies or calculate the value of similar publicly traded companies.

- Calculate relevant valuation multiples by dividing the value of each guideline company by a denominator such as revenue, operating income, EBITDA, or other value drivers.

- Select an appropriate valuation multiple(s) from the range of indicated multiples and multiply it by the subject company's financial fundamentals, indicating business value.

There are many nuances to valuing a business using the market approach, but these steps summarize the basic market approach framework.

Strengths of the market approach

A foundational text for in the business valuation community is Revenue Ruling 59-60, which defines fair market value as “the price at which the property would change hands between a willing buyer and a willing seller…”1 The market approach can provide a convincing indication of value because it is based on exactly that—an actual transaction involving people buying and selling similar businesses.

The market approach may also be more easily understood than other valuation approaches for readers who don’t have a background in finance. In the income approach, business value is estimated by discounting or capitalizing the benefit stream of a business. If the reader is not familiar with the estimation and application of income approach variables, they may find the market approach to be more understandable and therefore reliable. The income approach is also heavily reliant on projected future cash flows, an area of uncertainty and potential bias.

Even when the income approach is applied, the market approach can be used as an indicator of reasonability. Credibility is enhanced if a valuation analyst uses two or more different processes to get similar indications of value.

Weaknesses of the market approach

While one of the strengths of the market approach is how well it relates conceptually to the definition of fair market value, it also highlights a potential weakness of the market approach. Many transactions occur because the acquirers expect to achieve synergistic benefits from the transaction. These synergies may be priced into the transaction, potentially inflating the transaction price above fair market value. Therefore, it is possible for the market approach to indicate investment value rather than fair market value. It is also difficult to know what motivated a sale. Without knowing the intent of the buyers and sellers, it is difficult to determine whether a transaction reflects fair market value or investment value.

It is often difficult to locate companies that are reasonably similar to the subject company. People often start businesses because they see a need that isn’t being met—that is, there aren’t any companies like the one they want to start. The point of a business is to be different than its competitors. While differentiation is great for creating a competitive advantage, it makes it difficult to find similar companies. Even if a market supports multiple similar businesses, these companies may not have ever sold. As a result, valuation analysts often struggle to identify guideline companies.

Identifying guideline public companies has its own set of challenges. Publicly traded companies often diversify their operations to reduce risk. The lack of pure-play public companies may limit the number of guideline companies available to the analyst. Further, publicly traded companies are often significantly larger than privately held companies, posing additional comparability challenges.

Another common limitation when applying the market approach is the lack of data from completed transactions. Financial data is often incomplete as it may have never been disclosed by either party in the sale of a business. Much of the data necessary for the market approach is also from subscription-based databases. If analysts choose to forgo this cost, they may lack sufficient data to apply the market approach.

The consideration paid in completed transactions is another potential weakness in the market approach. Consideration may include stock of the acquiring party, earn-outs, non-compete agreements, and other items. Adjusting these to a cash equivalent can be a subjective exercise. And where there is subjectivity, there is room for error.

Another area of subjectivity and potential errors is in the selection of valuation multiples. When valuing a house, the price per square foot of the selected comparables is typically in a much narrower range than the range of multiples when valuing a business. Analyst judgement is required to select a valuation multiple from the reported range. Analysts may err by selecting a multiple that is not warranted by the subject company’s operational risk profile and/or historical and projected financial performance.

At a high level, the application of the market approach is a straightforward three-step process: (1) identify sales of similar companies, (2) calculate relevant valuation multiples, and (3) select and apply an appropriate valuation multiple.

The discussion above should provide high-level clarity as to the application of the market approach. Keep in mind the strengths and weaknesses of the market approach when formulating an opinion about the usefulness of this indication of value.

BerryDunn’s Business Valuation Group partners with clients to bring clarity to the complexities of business valuation while adhering to strict development and reporting standards. We render an independent, objective opinion of your company’s value in a reporting format tailored to meet your needs. We thoroughly analyze the financial and operational performance of your company to understand the story behind the numbers. We assess current and forecasted market conditions as they impact present and future cash flows, which in turn drives value. Learn more about our team and services.

1 Revenue Ruling 59-60, 1959-1 CB 237; Estate Tax Regulations §20.2031-1(b); Gift Tax Regulations §25.2512-1.

Skip to Main Content

Skip to Main Content